With new chip credit cards on way, here’s what consumers need to know

Techies are calling the upcoming shift in how we will use our credit cards at the store something like “dip the chip.” It’s not a bad way of explaining things. Instead of swiping our plastic, we’ll be able to slide or dip our chip-equipped credit cards at chip-enabled terminals at the register. You might see the new way of doing things as soon as the next time you shop at Target or another big retailer. A unique one-time code is generated every time a card with a chip is used, and a one-time code is hard for crooks to duplicate to make fake credit cards, according to card experts. Chips aren’t entirely new. They’ve long been used in Canada and all across Europe.

Techies are calling the upcoming shift in how we will use our credit cards at the store something like “dip the chip.” It’s not a bad way of explaining things. Instead of swiping our plastic, we’ll be able to slide or dip our chip-equipped credit cards at chip-enabled terminals at the register. You might see the new way of doing things as soon as the next time you shop at Target or another big retailer. A unique one-time code is generated every time a card with a chip is used, and a one-time code is hard for crooks to duplicate to make fake credit cards, according to card experts. Chips aren’t entirely new. They’ve long been used in Canada and all across Europe.

But the U.S. has been stuck in the swipe-and-sign mode for years. Beginning in October, though, some rules will change for merchants that will drive a shift into chip technology. A week or so ago, my credit card issuer sent me a notice saying that I should be receiving a new EMV Chip Technology card for my MasterCard by October. Other consumers already have chip cards in hand. Bank of America, for example, has been adding chip technology to its consumer credit cards since mid-2012 and started adding chips to debit cards last October. Bank of America said the vast majority of its debit card and credit card customers are expected to have cards with the microchip by the end of the year. Chase said it plans to convert more than 70% of its credit card and debit cards to chip technology by year’s end.

The bank is also upgrading its ATMs to accept chip cards. Some big-name retailers are rolling out new systems, as well. Target just finished setting up all of its stores to accept chip cards at its registers. Walmart and Sam’s Club stores began accepting chip-embedded credit cards last November. What do you need to know about those chips? 1. Will the magnetic stripe on the back go away? No. While major retailers are moving toward the chip terminals, many experts say smaller retailers are less likely to upgrade for some time. Doug Johnson, senior vice president of payments and cybersecurity policy for the American Bankers Association, said less than half of merchants with point-of-sale devices in the store are expected to have chip-enabled systems in place by year’s end. While some merchants say the costs are too high, Johnson and others noted that options are available at fairly low costs, such as $30 or $40, to handle chip technology for those who use computer tablet devices at the register.

The chip-and-sign devices, he said, are less costly than if we moved to a chip-and-PIN system. People will still sign for their purchases, typically, and not use a PIN with the chip credit cards. It’s still going to take time to get the chip cards into the hands of consumers, too. Stephanie Ericksen, vice president of Risk Products at Visa, said nearly 127 million — or about 18% — of all Visa cards at the end of July were chip-enabled cards. Those numbers will grow as we move into the holiday shopping season. Some banks are reissuing chip cards as credit cards reach expiration dates; others are rolling out cards in batches. The industry expects that about 63% of credit and debit cards should contain EMV chips by the end of 2015. That’s expected to increase to 98% by the end of 2017, according to the Payments Security Task Force, which was formed in early 2014 and includes groups in the electronic payments industry, including banks, retailers and others. 2.

What happens if I don’t get a new chip card soon? “Nothing really,” said Gerri Detweiler, at Credit.com . If you don’t get a new chip card by this fall, she said, you will still be able to use your current card. Remember, the consumer’s liability for fraudulent purchases does not change. You’d still have the same protections. The chip technology focuses on in-store purchases and cutting down on fraud involving fake cards. It does not address online purchases, but other technology down the line would offer more secure online purchases. 3. How do I know if I have a chip card?

Look at the front of your card on the left-hand side. Do you see small metallic gold- or silver-looking rectangle, possibly above the first four digits of your card number? That’s the chip. The chip only provides extra security with a chip-enabled device. If you swipe, the extra level of security is not present. 4. What kind of mishaps can happen with the new chip cards? Consumers have to learn a new payment process, but it’s not really rocket science. “It’s a quick transaction,” said Randy Hargrove, a spokesman for Walmart in Bentonville, Ark. “Once you do it the first time, it’s certainly an easy transaction.”

Consumers just need to get used to doing things slightly differently at the store. Some stores once allowed you to swipe your card long before the clerk rang up the entire cart. The chip system is different. You need to wait to insert the card in the reader until all your items are rung up. The reason? The transaction itself is part of the coding process. “You have to wait until everything has been totaled up,” said Michael Moesser, director of payments practices at Javelin Strategy & Research. You also have to wait a while for the process. Some clerks have had to tell customers to keep the card in the reader until they hear a beep or get another signal. Some shoppers think you can put the chip card in and pull it out of the reader quickly, and that’s not the case. You must leave that card in the reader until prompted to take it out. You’re going to sign for the purchase, if a signature is required, while the card is in the reader, too. Moesser is concerned that some consumers might forget to take the card out, particularly if they’re in a hurry. But again, terminals give off a beep or might flash to let you know the transaction has been authorized and to remember to take the card. Also, the chip isn’t going to help right now with online sales. “The EMV chip technology is intended to combat card-present fraud in stores, specifically counterfeit cards,” Moesser said.

“Unfortunately, the chip technology does not apply to online purchases, where the physical card is not used in the transaction. Card issuers and banks are working with merchants to promote widespread adoption of existing security features, as well as develop new ones to combat online credit card fraud,” Moesser said. Another possible point of confusion: Right now, some terminals at stores look like they can accept a chip but do not have chip functionality yet. Some of those systems will be turned on later. Various banks, including Bank of America, are sending out step-by-step instructions with the card or listing tips online.

What is this October deadline that I’m hearing about in the news? Beginning Oct. 1, merchants that have not updated point-of-sale devices to recognize chips will be held liable if there is fraud at the register in the store if the bank has issued cards with chips. Whoever has the older technology is liable for fraud. If both the bank and the retailer have updated their technology, the liability falls back to the bank. Right now, the bank assumes that liability.

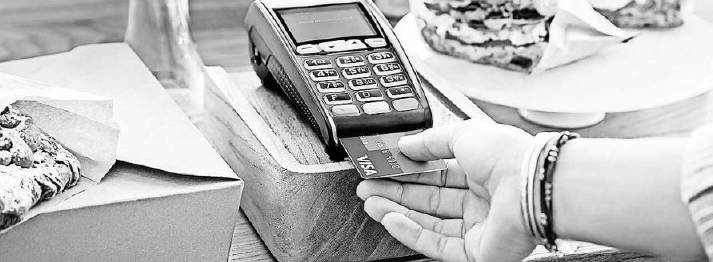

VISA Shoppers must wait until all purchases are rung up before inserting a card into a chip reader.

MARTIN MEISSNER, AP Chip-enabled cards will still have magnetic strips on the back.

Susan Tompor @tompor stompor@usatoday.com USA TODAY

Attend the CED Solutions 5-day courses: Technical installation and configuration of Windows 10 and Deploying and Managing Windows 10 in October.

Start your IT career with the CompTIA A+, Network+, Security+ at CED Solutions today!

CED Solutions is a Cisco Learning Partner, Microsoft Gold Learning Partner and the #1 location for Microsoft Certifications in North America for the last 6 years combined. CED Solutions is a CompTIA Partner, EC Council Partner, and many others and is one of the largest providers of training in North America. The Atlanta facility provides IT training for up to 300 students per day, with separate buildings dedicated to training. CED Solutions provides training for thousands of students per year and students take up to 800 certification exams every two weeks.

CED Solutions provides training and certification for MCSD: SharePoint 2013 Applications Developer; MCSE: SharePoint 2013; Cisco CCNA; Cisco CCNP; Cisco CCNA Security; Cisco CCNP Security; Cisco CCNA Voice; Cisco CCNP Voice; Microsoft MCSA: Windows 2012 Server; MCSA: Windows 2008 Server; MCSA: SQL 2012 Server; MCSE: Business Intelligence SQL 2012 Server; MCSE: Data Platform SQL 2012 Server; MCSE: Desktop Infrastructure Windows 2012 Server; MCSE: Server Infrastructure Windows 2012 Server; MCPD: 6 Cert Visual Studio Developer; MCSD: Windows Store Apps C#; MCSD: Windows Store Apps HTML5; IT Healthcare Technician and many more.

CED Solutions, LLC, www.cedsolutions.com, info@cedsolutions.com, (800) 611-1840